I was studying for my PhD in the 1960s. One day the Dean of Graduate Studies, at a welcoming session, added that we should worry only about studying. If we had concerns about money or anything else, we should go and see him. I really found America, I thought! I could not believe my ears. I went immediately to see him and asked for a raise in my research grant. And he gave it to me!

I was studying for my PhD in the 1960s. One day the Dean of Graduate Studies, at a welcoming session, added that we should worry only about studying. If we had concerns about money or anything else, we should go and see him. I really found America, I thought! I could not believe my ears. I went immediately to see him and asked for a raise in my research grant. And he gave it to me!

Many years have gone by since those naïve days full of hope and pleasant surprises. I changed with the country. Slowly but steadily, I learned to appreciate its grandeur, its many faceted aspects, its many ways to create wealth.

The toughest period for me were the 1970s. I was struggling like everybody else. War, inflation, soaring interest rates, discontent, young people going to Canada to avoid the draft, the Japanese opening production plants challenging mighty Detroit with their robots, the sorrowful decline of the dollar which mirrored exactly the inflation differential between the US and, say, Germany or Japan, the sharp back-to-back recessions.

People were telling me cars were rusting so quickly to keep the economy growing. Cars were so big when compared to the tiny European ones. I did not realize then how much of the purchasing power was created by leverage.

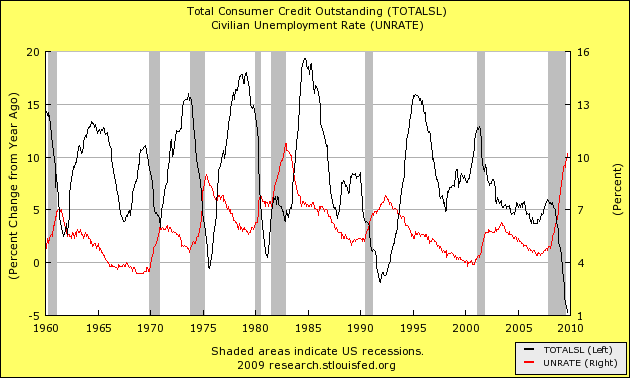

One of my first thoughts was that the banks owned consumers – or 70% of GDP. The sophistication of the credit markets and work ethics were the main reason for this availability of credit.

The pendulum never stands still. It swings slowly and steadily. Banks found new ways of lending and leveraging assets. Until everything cracked.

Now consumers are realizing debt is not a one-way street. Banks made similar miscalculations.

The pendulum is swinging back. We do not know when it will stop. But you can rest assured consumer spending is not going to be 70% of GDP in the future. Only a strong dollar will flag the return of the consumer and strong economic growth. It will signal we have learned to be competitive again as we were in the 1950s and 1960s.

To find out more about my in depth views of the markets and my strategy just visit our website https://www.peterdag.com/ where you can review The Peter Dag Portfolio. You can also call me at 1-800-833-2782 to discuss your specific money management needs.

I will be happy to speak to your investment group on how the business cycle impacts investment strategies and the choice of asset classes.

George Dagnino, PhD

Editor, The Peter Dag Portfolio. Since 1977

Ranked Top Market Timer in 2009 by Timer Digest

Disclaimer. No material here constitutes "investment advice" nor is it a recommendation to buy or sell any financial instrument. Actions you undertake as a consequence of any analysis, opinion or advertisement on this site are your sole responsibility.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)